Disclosure

We are short shares of FIVE. Please click here to read full disclosures.

We believe that Five Below (FIVE) is highly overvalued. FIVE is a specialty value retailer that offers merchandise targeted to teens, pre-teens and their parents in a concept that we view as a glorified dollar / toy store. Its valuation multiples of 3x+ LTM revenue and 25x LTM EBITDA are far too high for a company with mediocre same-store sales growth operating in the brutally competitive discount segment of the retail industry. Same-store sales growth (SSSG) has declined dramatically over the past three years, with SSSG for Q4 2013 falling to an anemic 0.4% and overall forward year guidance projected to be a modest 4%. Additionally, we expect the company’s long-term margins to be pressured by the wave of competition flooding the discount retail sector, whether it be due to the 5% to 7% annual unit expansion of Dollar General, Dollar Tree or Family Dollar, or the 2,000+ Walmart Express small-format stores expected to open over the next five years; additionally, discount retailers rarely boast impressive profit margins due to their lack of brand name products. Finally, FIVE’s catalogue is biased towards trendy/fad items that are targeted for a fickle teenage demographic and its sales are disproportionately weighted towards the holiday season, factors which both translate to increased volatility in year-to-year results.

For all the aforementioned reasons, we think that the current $2.0 billion market cap being assigned to Five Below, a company that generated only $80m of EBITDA and $40m of net income in fiscal 2013, faces substantial downside over the coming year. Indeed, it was no surprise that when the company released its Q1 earnings last week, and both beat analyst estimates and raised guidance, the stock ended the day down 4%. The market has seen a violent re-pricing for high-flying momentum stocks over the past few months, with former momo darlings like SPLK, CSLT and FEYE down more than 50% from their peaks. Egregious valuations of recent IPOs that were inflated by thin floats and easy-to-beat sellside estimates have a seen a downward revision since mid-March. Many of these momentum names have beat estimates and raised guidance in the most recent quarter, but have still seen their stocks fall after earnings. Companies that have underperformed expectations have routinely witnessed their stocks plummet more than 20%.

We think FIVE has yet to fully participate in the much-deserved momo correction.

At current premium multiples, investors are assuming FIVE experiences no missteps in executing its high-growth strategy. A valuation of 25x LTM EBITDA implies substantial margin expansion, 10%+ SSS growth, and a maintenance of 20%+ unit growth for many years to come. However, we believe that FIVE’s 13% EBITDA margin is already at elevated levels; we note that its SSS growth has already fallen below 5%, let alone the 10%+ level that its nosebleed valuation implies; and we believe that 20%+ unit growth will be difficult to execute effectively as FIVE’s store base becomes larger and larger. Throughout this and future articles, we will elaborate on other fast-growing retailers that have expanded too quickly in order to justify lofty valuations, such as Francesca’s Holdings (FRAN), only to experience declining sales per square foot and negative same-store sales growth, which have in turn triggered valuation cuts of 50% or more.

To value FIVE, we discuss a comparable companies analysis that compares FIVE to other fast-growing emerging retailers, as well as dollar stores. FIVE’s stretched multiples stand out even when compared with other overhyped momo retailers. When matched with other dollar stores, FIVE’s valuation is clearly an outlier, and although investors may claim that FIVE is at a different stage in its lifecycle than perhaps a Dollar General, we question just how different FIVE’s business model really is from other discount retailers.

Additionally, we present a highly optimistic 10-year discounted cash flow analysis to supplement our comparable companies analysis. Our DCF yields a valuation for FIVE of approximately $23 / share, well below the current price of $35. Even in a scenario where FIVE triples its store count and quadruples revenue and EBITDA, shares would be 35% overvalued based on our analysis.

|

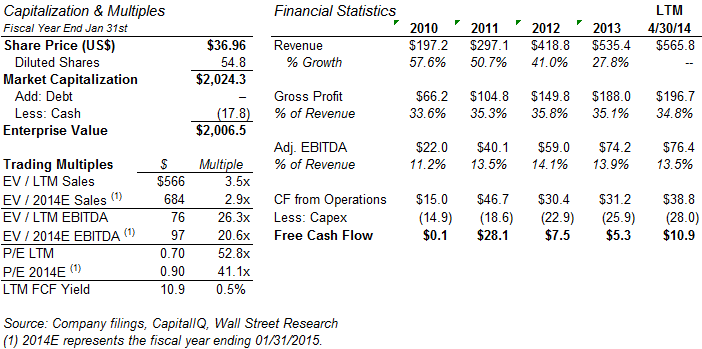

Capitalization and Financial Snapshot |

|

Gross Overvaluation Relative to Peers and other Retail Stocks

FIVE’s share price of $35/share implies a lofty valuation of 3.4x LTM revenue, 25x LTM EBITDA and 50x LTM P/E. On a forward basis, FIVE trades at 2.8x FY14E revenue, 20x FY14E EBITDA and 39x FY14E P/E. On almost any metric, FIVE looks expensive, especially when compared to other, arguably more successful, retailers. Lululemon, which has a premium brand name, better margins, and higher SSSG, trades at a 34% and 43% discount to FIVE’s 2014E EV / EBITDA and P/E multiples, respectively. Conn’s Inc, a specialty retailer focused on electronics and appliances, had SSSG of 27% in Q1’14, is expected to increase revenue by 27% in 2014, and has higher EBITDA margins than FIVE, yet it also trades at a significant discount relative to FIVE.

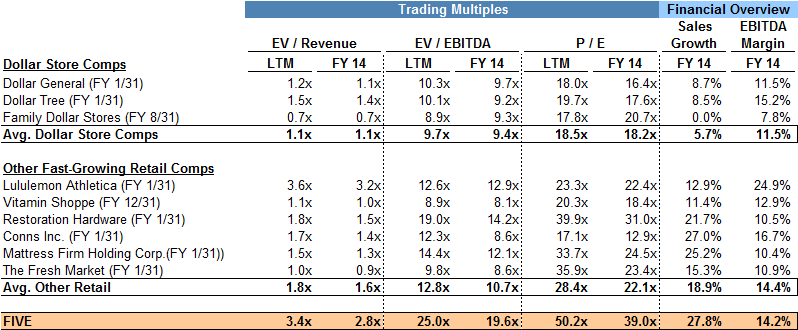

Below is a comparable companies analysis that compares FIVE to two comparables sets: (i) other dollar stores and (ii) other fast-growing retailers.

|

Public Comparables – Trading Multiples and Financial Overview |

|

|

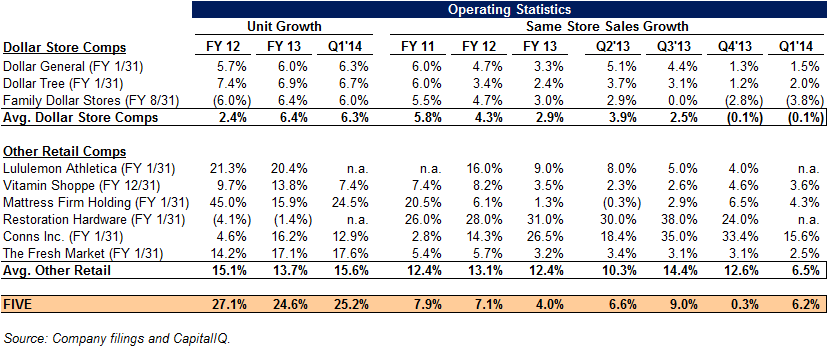

Public Comparables – Operating Statistics |

|

When compared with other fast-growing retailers, FIVE’s steep valuation multiples stand out. For instance, Restoration Hardware (RH) is expected to grow 2014 revenue by 22%, and its 2013 same-store sales growth was a resounding 31%. The company is also benefiting from a showroom-oriented business model like WSM, whereby the company is rapidly increasing its online sales through online advertising and social media rather than expanding its units. Yet RH’s EV / EBITDA multiple is 30% lower than FIVE’s.

When compared to other dollar store operators, FIVE’s revenue multiple is three times higher than the average of the comparable set, and its forward 2014E EV / EBITDA and P / E multiples are more than twice as high. We expect FIVE’s growth and margin metrics to moderate faster than sellside analysts think. Maintaining 14% EBITDA margins and elevated same store sales growth as a discount retailer will become much harder when the company operates 500+ stores as compared with its current 323-store base, especially when the company is increasing unit growth at a 25%+ annual clip. We think it’s probable that execution issues, such as poor site selection, disadvantageous leases, and off-trend merchandising, will hamper FIVE’s growth and margins in the near- to intermediate-term.

Over time, we believe the valuation gap between FIVE and its peers will narrow, as investors will realize that FIVE’s premium valuation is unwarranted.

Declining Same Store Sales Growth Suggests 20+% Revenue Growth Unsustainable

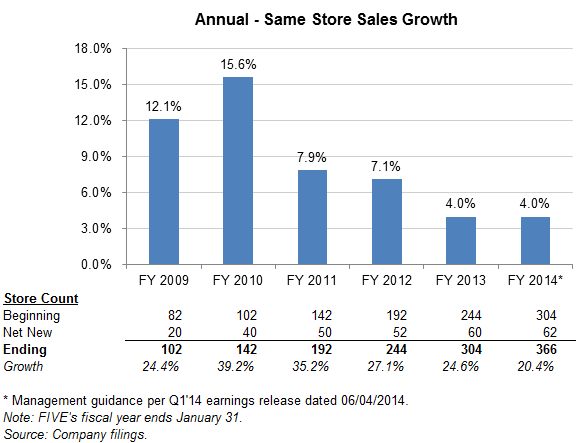

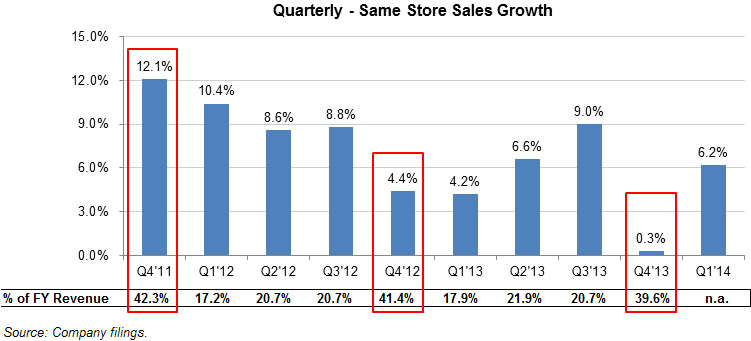

At first glance, FIVE’s FY 2009 – 2013 revenue CAGR of 44% certainly seems impressive. However, most of this growth was driven by new store openings. From FY 2009 – 2013, FIVE opened 222 net new stores (CAGR of 31%) and expects to open 62 more in FY 2014. Over the same period, same store sales growth (SSSG) declined from a high of 15.6% in FY 2010 to 4.0% in FY 2013. For FY 2014, management projects that same store sales growth will be flat at 4.0%, implying no improvement from FY 2013.

Notably, FIVE’s SSSG in the fourth quarter has been on a declining trend since FY 2011. The fourth quarter is the most important quarter of the year for many retailers due to the holiday season. This is especially true for FIVE as the fourth quarter represented 42%, 41% and 40% of total sales for the fiscal years 2011, 2012 and 2013, respectively.

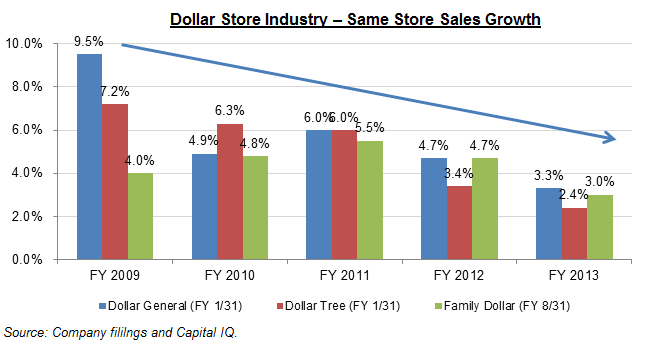

The deceleration of SSSG is a common trend in the dollar store industry. SSSG for Dollar General, Dollar Tree and Family Dollar has declined significantly since FY 2009. Extrapolating from this trend would suggest that long-term growth rates for this industry would be in the low single-digits. While FIVE continues to grow revenues by 20-30% (31% y-o-y growth in Q1’14), the growth has been fuelled via adding new stores, which requires upfront capital, rather than same store sales growth.

Margins at Elevated Levels and May Contract Long-Term

Investors in FIVE are bullish on the company’s growth prospects, highlighting FIVE’s profitability and operating metrics. Retail however is a commoditized and cutthroat industry, and while FIVE may have carved out a unique niche as a teen and pre-teen focused dollar store operator, we question its ability to command sector-leading margins as it expands its store base.

FIVE has minimal sustainable competitive advantages. Despite operating in a commoditized industry, it is not a low-cost competitor, like a Wal-Mart or Costco. It does not have strategic real estate locations, unlike many of the dollar stores, which had first-mover advantages in picking up prime dense-population locations. It does not have unique product sourcing capability. Nor does the firm have a brand name or long-standing customer relationships and customer data (one of the few things keeping customers coming to retailers such as JC Penny and Sears). Its unique strategy of focusing on teenagers and their parents differentiates the retailer, but we don’t think this will be enough to allow FIVE to maintain sector-leading margins over the long-term.

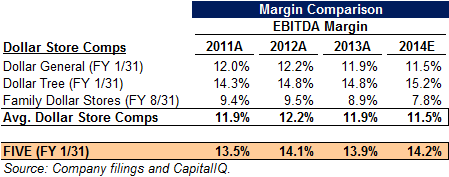

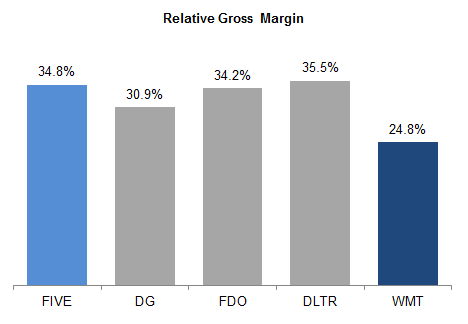

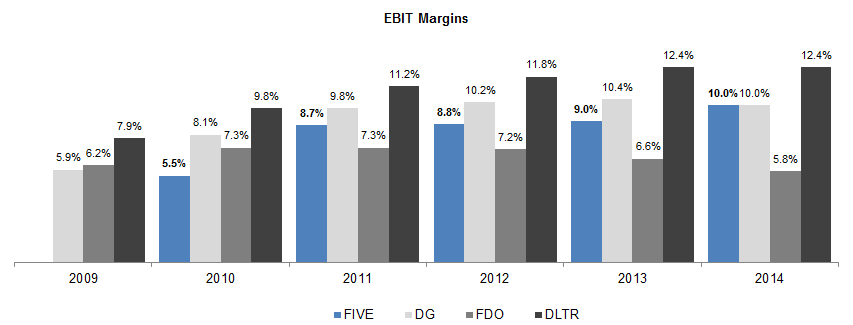

Below is a comparison of FIVE’s margins to competitors:

As we can see, FIVE currently boasts a higher margin than both Dollar General and Family Dollar, by over 250 basis points as compared to Dollar General and at nearly double the EBITDA margin of Family Dollar. We don’t think this is sustainable.

What FIVE offers is simply a product assortment and a price point. And these are things that any retailer can quite easily replicate. Competitor commentary indicates that traditional discount retailers are already adding products at the $1.00 to $5.00 price point. For example, Dollar Tree has been rapidly expanding its Deal$ store format, which sells products higher than its traditional $1.00 price format. It should be noted that Dollar Tree’s Deal$ format is already quite sizable at ~220 locations, compared to ~300 for FIVE.

“Another key component of our growth strategy is the expansion of Deal$, Dollar Tree Canada, and Dollar Tree Direct. Our Deal$ format extends our ability to serve more customers with more categories and increases our unit growth potential. Deal$ stores deliver low prices on everyday essentials, party goods, seasonal and home product. By lifting the restriction of the $1 price point at Deal$, we’re able to serve more customers with more products at value prices every day. We ended the quarter with a total of 217 Deal$ stores and growing.” – Bob Sasser, Dollar Tree CEO, Q1 2014 Transcript

Perhaps even more troubling is the recent decision by Dollar General to add more products at a higher price point in order to capture additional consumer wallet share. Dollar General is currently the largest discount convenience retailer in the United States, with over 11,000 locations. While Dollar Tree decided to create an entirely separate brand (“Deal$”) for its stores that carry a wider assortment of goods, Dollar General’s decision to allow > $1.00 price products into its existing stores could represent a significant threat to FIVE’s locations, many of which are adjacent to Dollar General’s existing stores.

Source: Bloomberg

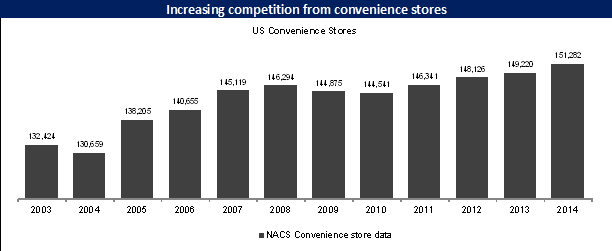

If the increased competitiveness of dollar stores is not dangerous enough, the US convenience store industry has also seen a very significant expansion in terms of both units and square footage and is now creating considerable competition in terms of consumables.

However, these competitive threats are likely dwarfed by the potential threat from Wal-Mart Neighborhood Market and Wal-Mart Express.

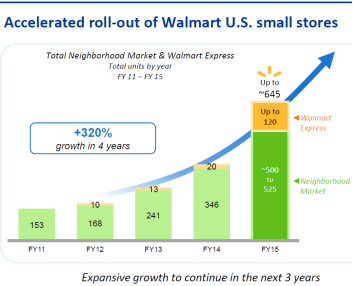

Investors are Going to be Blindsided by a Looming Threat… Wal-Mart Neighborhood Market

FIVE’s success has largely been a function of identifying a unique inventory assortment and making it available in a small, convenient and local store format. Investors have largely assumed that FIVE has a unique market position since many of its inventory products are not widely available at the other local discount retailers (such as formats owned by FDO, DG, DLTR) because FIVE’s discount competitors were largely focused on selling consumables rather than variety, house ware and seasonal goods.

That is about to change with the broad introduction of Wal-Mart’s new small-format concepts: Wal-Mart Neighborhood Market and Wal-Mart Express (collectively referred to as “Wal-Mart Small Format” or “WSF” in this report).

WSF’s are particularly worrisome competitive threats for the discount retail industry for four key reasons:

- Wal-Mart sell products for a far lower profit than competitors; this will decimate margins in the industry

- Wal-Mart will likely take share; it has greater brand recognition, foot traffic, and turnover

- WSFs will offer a wider assortment of products and services given their larger footprint

- WSFs are not only a retail format, but a shipment node for the lower cost Wal-Mart supercenter stores

For the past several years, Wal-Mart has been experimenting with smaller-format concepts as well as online delivery business models. It has been trying to understand what store size, product assortment and price points will allow them to profitably enter the local discount retailing space, and how these local stores can be used to augment and enhance their online strategy.

Finally, after several years of testing and adaptation, the company has finally settled on a business model it is happy with, and Wal-Mart has indicated that 2014 is the start of an aggressive expansion of its WSF stores, with the planned opening of at least 250 of these stores in the coming year, with hundreds more to follow in coming years.

Source: Wal-Mart investor day presentation, March 2014

“We’ll add 270 to 300 new small units this year. That includes 160 to 180 Neighborhood Markets, 110 to 120 Express formats. This will allow us to gain more of a convenient shopping trip for our customers in what they want… There are something like, I think, 11,000 new small stores that have been put out in the U.S. in the last 3 years that we think have impacted that… We think it’ll be a very powerful vehicle for the customer experience with this convenience and be able to combine that digital and that physical for that customer.” –Source: Charles Holley, CFO, March 2014

While the typical Wal-Mart supercenter is nearly 200,000 square feet, the Wal-Mart Neighborhood Market and Wal-Mart Express stores are approximately 40,000 and 12,000 square feet in size, respectively, a significantly larger format than the typical discount store size of between 5,000 and 10,000 square feet. These stores will have a large enough footprint such that, in addition to offering grocery, pharmacy, and other key recurring-revenue consumable products (which is the bread & butter of most discount retailers), the WSFs will also have sufficient space to offer housewares, party, sporting goods and other seasonal selective merchandise which will be in direct competition with FIVE.

The mere footprint expansion does not capture the full scale of the competitive threat.

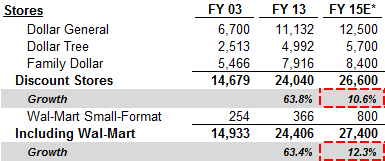

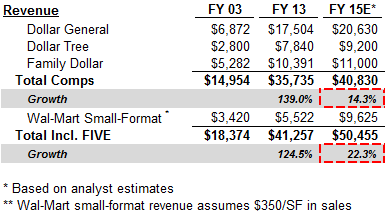

Investors may look at Wal-Mart’s modest unit count and assume that it is only modestly nudging the total industry’s unit growth over the coming couple of years. However, when one looks at the projected increase in competition from a revenue standpoint, one can see that the WSF stores’ total revenue expansion is a far more serious threat. Simply put, FIVE is competing in a commoditized industry where nearly every competitor plans to aggressively grow unit count and even more aggressively grow revenue, yet analysts expect margins and profitability to remain constant despite the world’s most sophisticated and aggressive retailer entering the market?

|

Wal-Mart is Going to Quickly Become a Very Major Competitor in the Discount Retail Industry |

|

|

|

|

This doesn’t seem to make sense, particularly when one looks at Wal-Mart’s far lower margins, and store-level turnover metrics.

|

Wal-Mart Sells Products at a Far Lower Price… |

… by Utilizing its Real Estate More Efficiently… |

Wal-Mart pricing is disruptive for the entire discount retail industry |

Wal-Mart will use its brand recognition, superior slate of services, and larger format to grab share

|

The primary concern is that Wal-Mart, simply put, is an incredibly aggressive competitor that is willing to earn less on each sale than its competitors. They make up for this lower profit by turning their inventory faster, and utilizing their real estate more efficiently through better sales per square foot.

The entry of Wal-Mart is not just a threat for FIVE, but for the entire discount retail market in general. The copious profits, impressive 10%+ EBITDA margins, and fantastic returns on equity that the industry has enjoyed for the past decade are likely to deteriorate when Wal-Mart’s begins to disrupt the industry.

FIVE’s Retailing Model is Inherently More Risky than Other Discount Retailers Due to Dependency on Holiday Season

Many research analysts compare FIVE to other discount retailers such as DG, FDO and DLTR. However, there are fundamental differences in FIVE’s business model which make these comparisons quite risky and misleading.

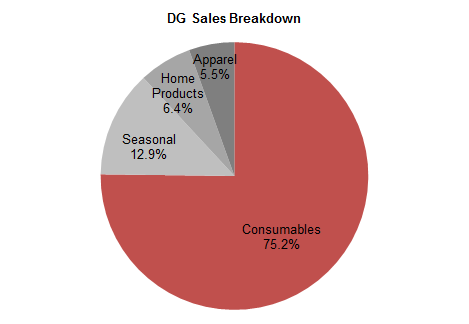

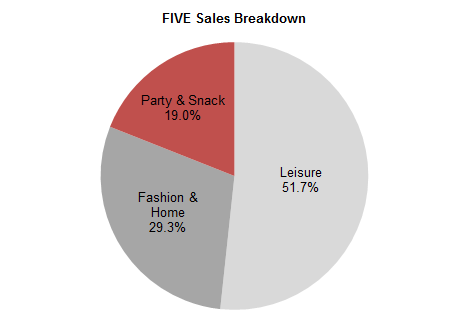

While other discount store retailers focus heavily on providing consumable merchandise, such as grocery and household consumables, FIVE is more heavily weighted towards leisure items and house ware. Discount retailers often focus on minimizing costs, improving efficiencies and sourcing the lowest-cost everyday household items; in contrast, FIVE’s merchandising team must continue to accurately predict customer tastes and trends, much like a fashion or furniture retailer. Thus, FIVE’s merchandising mix is significantly riskier than that of a consumables retailer such as Dollar General.

|

DG Sales are Largely Recurring Consumables… |

… Whereas FIVE Sales are “Trend” |

|

FY 2014 Revenue: $17.5B |

FY 2014 Revenue: $0.5B |

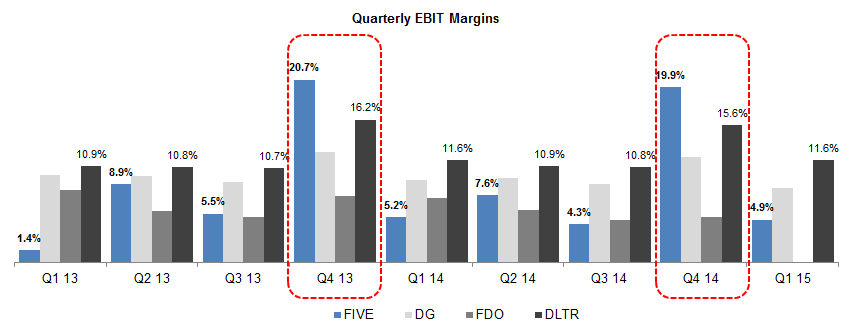

Another important data point is FIVE’s heavy dependence on the holiday season for sales. This important distinction is not as evident when one looks at annual figures; however, when looking at quarterly financial results, it is quite evident that FIVE is disproportionately reliant on the holiday season. In fact, the company is barely profitable for the other three quarters of the year.

|

FIVE EBIT Margins Appear Normal on an Annualized Level… |

|

While DG, FDO and DLTR generate a relatively steady, recurring engagement with their customers through selling convenient consumable merchandise, FIVE is far more dependent on selling “trend” inventory for holiday gifting season. Though this strategy can yield outsized margins when successful, the risks to investors from even one poor Christmas season can be significant. Particularly cold weather, as in 2013, or poor holiday merchandising in a given year can adversely impact FIVE far more than its peers.

|

… but Quarterly Results Show that FIVE is Really a Holiday Retailer |

|

Thus, due to FIVE’s heavier reliance on non-recurring items and holiday sales, its revenue and profits are less predictable than its discount retailing peers. Seasonal weather or poor execution during the holiday season can have a particularly pronounced impact on FIVE’s profitability. FIVE’s dependence on predicting customer demand for seasonal items makes them more akin to a lower-multiple fashion retailer such as a GPS (which trades at 14x forward P/E) rather than a recurring-revenue, low-cost consumable merchandise company such as a Costco (23x forward P/E) or DG (18x forward P/E).

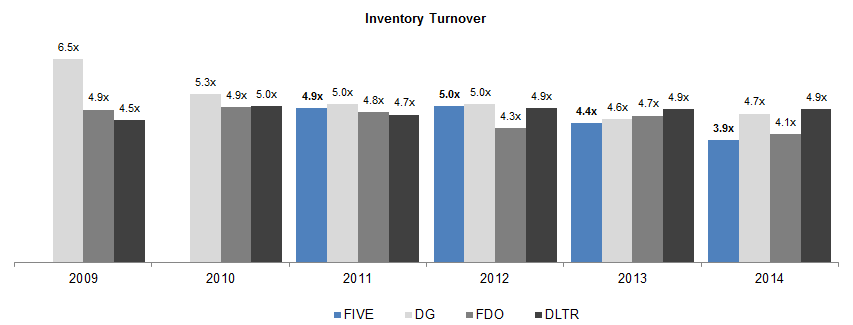

Low Inventory Turnover a Cause for Concern

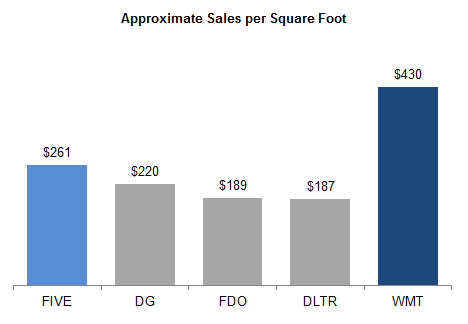

When comparing FIVE’s inventory turnover metrics, cost basis (SG&A as % of revenue) and overall retail efficiency (sales per square foot, SG&A per square foot), FIVE’s metrics are quite poor compared to other dollar stores, and particularly poor when compared to large competitors such as Wal-Mart, Costco, etc.

Given that FIVE is a holiday-dependent retailer, its declining inventory turnover is particularly troubling. For example, for a retailer that sells household items and consumables (such as a CVS), the vast majority of their store-front sales are non-perishable inventory items. If a stick of makeup doesn’t sell in one quarter, it can often be sold in the next.

However, for a retailer that sells perishable items, or in FIVE’s case, holiday-dependent “seasonal” purchases, a lost sale may not be recovered, at least for an entire year. This heightens the risk of taking a significant loss on inventory. FIVE’s recent inventory trends look particularly troubling.

|

FIVE’s Inventory Turnover is Falling, Which is Particularly Risky for a Holiday-Dependent Retailer |

|

Declining inventory turns raises the danger of inventory obsolescence at FIVE, which would compress margins and further call into question the company’s 50x LTM P/E and 39x 2014E P/E multiples.

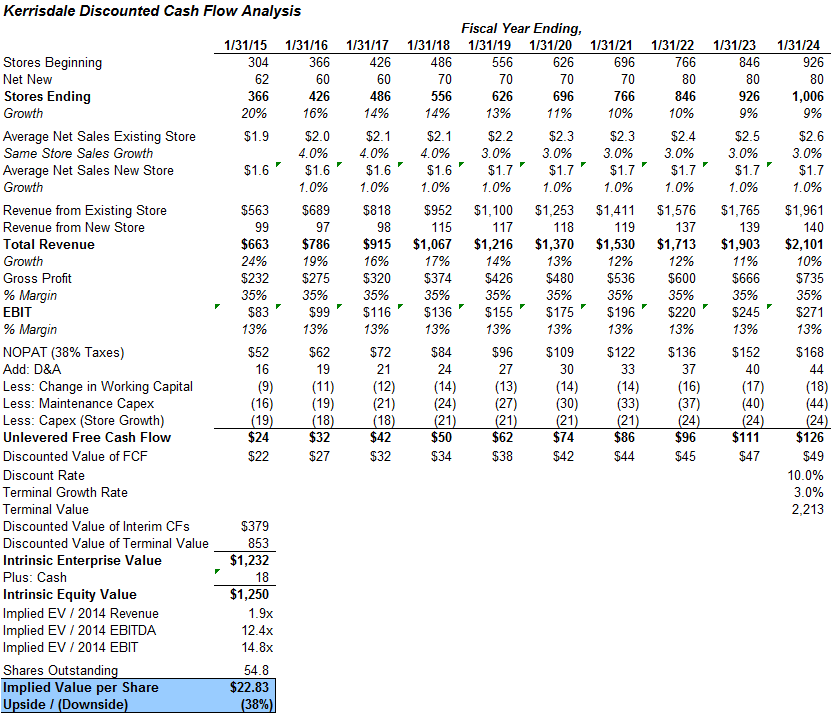

Highly Optimistic Discounted Cash Flow Analysis Implies 40% Downside

While we highlighted FIVE’s significant overvaluation relative to other retail companies, our highly optimistic DCF analysis further exposes FIVE’s current stock price vulnerability. Under our generous assumptions, we arrive at a share price of $23, 35% below where the stock closed on Friday. This valuation implies a more reasonable 11x 2014E EBITDA multiple, far below the current 20x multiple and in-line with high-growth retail stocks. Under this illustrative 10-year scenario, we assume that FIVE more than triples store count, quadruples revenue, and EBITDA and that SSSG stabilizes at 3.0% per annum. Our other assumptions include the following:

- Net new stores of 60 per year, 70 per year starting in 2018, 80 per year starting in 2022

- Gross margins of 35% and EBIT margins of 13% throughout projection period

- Maintenance capex growing at new store rate

- Store growth capex of $0.3 million per store

- Discount rate of 10%; terminal FCF growth rate of 3.0%

Even in our highly optimistic scenario where we project FIVE to grow revenue and EBITDA at a CAGR of 15%, the analysis reveals significant downside. Further, this scenario illustrates a best case scenario where FIVE has absolutely no missteps in growing store count, is able to manage volatility in sales of products that are inherently trendy, and executes its strategy to perfection. We believe that a tempered version of this scenario would further highlight FIVE’s current overvaluation and suggest even more downside.

Conclusion

In closing, we applaud FIVE’s management team for growing their concept to the current scale. However, we believe that the company’s market valuation is unjustified given the sharply declining SSSG trend, increasingly competitive discount retailer landscape, faddish nature of FIVE’s products, and its dependence on the holiday season. In light of these risks, and based on peer retail firms’ significantly lower valuations and our DCF analysis which suggests a much lower valuation, we believe that fair value is significantly below the current share price.

In future articles, we will discuss how many emerging retailers don’t live up to expectations, and how the retail landscape is littered with fast-growing concepts trading at 20x+ EBITDA in early years, only to see stock prices skid as execution issues, competition, cannibalization and limited total addressable markets lead to weakening sales per square foot trends, same store sales growth and margins in later years. We’ll also discuss how even some of the most successful concepts in the retail and restaurant sectors never traded at the lofty valuation multiples currently ascribed to Five Below.

Add New Comment