Five Below, Inc. (FIVE) Part 4

Recent Earnings for The Container Store and Potbelly a Warning for FIVE Shareholders

Disclosure

We are short shares of FIVE. Please click here to read full disclosures.

Introduction

Over the past several weeks, we have written a multi-part series about the perils of investing in specialty retailers, particularly those in undifferentiated formats. We strongly encourage readers to review our first three articles on Five Below (FIVE), each highlighting a different aspect about the risks of the specialty retail sector.

- Part 1: Five Below, Inc.: 50x P/E Too Rich For Xmas-Driven Discount Retailer highlights competitive risks in specialty retail

- Part 2: Five Below, Inc.: The Many Parallels With Other Overhyped Emerging Retailers That Have Disappointed Investors highlights how the specialty retail sector, as a whole, consistently disappoints investors due to unforeseen competition. In this article, we specifically highlight TCS and PBPB as specialty retail disappointments.

- Part 3: Five Below: New Morgan Stanley Initiation Relatively Lukewarm to FIVE’s Valuation highlights how investors risk permanent capital loss due to the unrealistic valuations paid for retailers.

In our multi-part series, we have discussed how investors repeatedly overvalue specialty retail concepts, often erroneously assuming that these companies can sustain high same-store sales growth and unit growth for long periods of time. In fact, more often than not, successful concepts are quickly copied or lose sales as customer preferences change. Generally, weakness in same-store sales growth (SSSG), particularly for specialty retailers with high valuations, is a leading indicator for potential valuation corrections.

This past week, two retailers we outlined in earlier articles saw their share prices decline significantly following disappointing earnings announcements. The first was The Container Store (TCS) which, despite only a modest reduction in guidance, fell as much as 15% after reporting Q1 earnings, and is now down nearly 40% year-to-date. The other recent IPO we highlighted was Potbelly’s (PBPB), which saw its shares fall nearly 25% after reporting preliminary Q2 earnings, and is now down 54% year-to-date. In both cases, SSSG has continued to trend down and failed to meet consensus estimates.

The recent events around TCS and PBPB offer FIVE investors a forewarning: positive sentiment on specialty retailers can quickly deteriorate after small hiccups, leading to significant valuation declines. We continue to believe that FIVE’s shares are materially overvalued, and that its recent declining SSSG trend, combined with hostile competition within the discount retail sector, may lead to an eventual share price correction as profitability and/or growth fail to live up to shareholders’ high expectations.

TCS and PBPB: Prime Examples of Specialty Retailers That Have Disappointed Shareholders

TCS and PBPB have followed similar trajectories as public companies and highlight the risks investors take when overpaying for promises of growth from emerging retailers. TCS and PBPB are recent IPOs that were heavily bid up by investors excited by a unit-growth story. Both offer formats that are differentiated to a degree but are nevertheless subject to brutal competitive landscapes: furniture retail and sandwich shops. Both entered the year trading at valuations that left little room for error, with multiples inflated by IPO hype and sellside analysts who were anchored to the aggressive estimates and multiples they assigned to the companies in their post-IPO initiating coverage reports. Both concepts began showing declining growth in same store sales – a typical precursor for emerging retailers poised to experience severe multiple contractions. Finally, both stocks have been tremendous disappointments for shareholders this year.

FIVE shares many of these commonalities with TCS and PBPB. Like these two comparables, FIVE is a recent IPO trading at nosebleed valuation multiples due to an aggressive unit-growth story. FIVE also operates in a difficult competitive landscape — discount retailing — and has recently witnessed declining same store sales growth over the past few years.

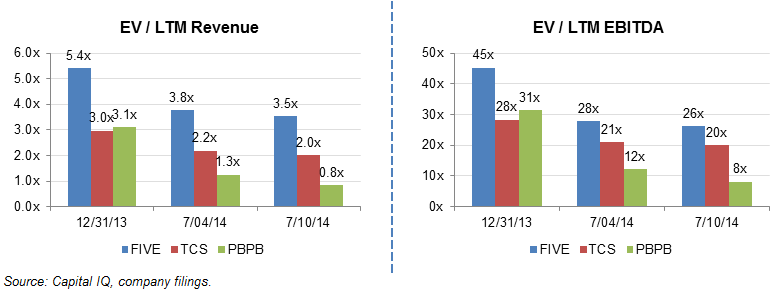

Year-to-date, valuations for TCS and PBPB have declined dramatically. TCS’ EV/EBITDA declined from 28x on 12/31/13 to 20x as of 7/10/14. PBPB’s EV / EBITDA has declined by 75%, dropping from 31x on 12/31/13 to 8x on 7/10/14. FIVE’s valuation has also declined, but to a much lesser extent than TCS’ and PBPB’s, and we believe the downward momentum will continue.

|

FIVE is Even More Overvalued than Either TCS or PBPB Before Their Recent Price Collapses |

|

TCS’ Precipitous Drop Exposes Vulnerability of FIVE’s Valuation

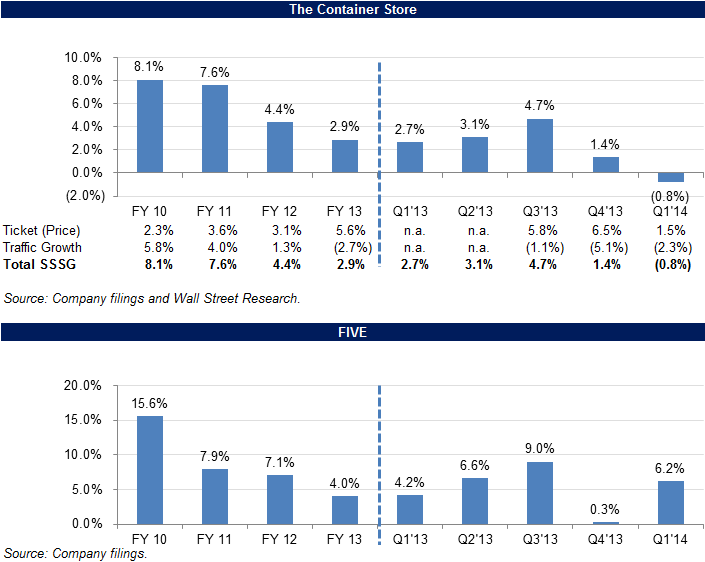

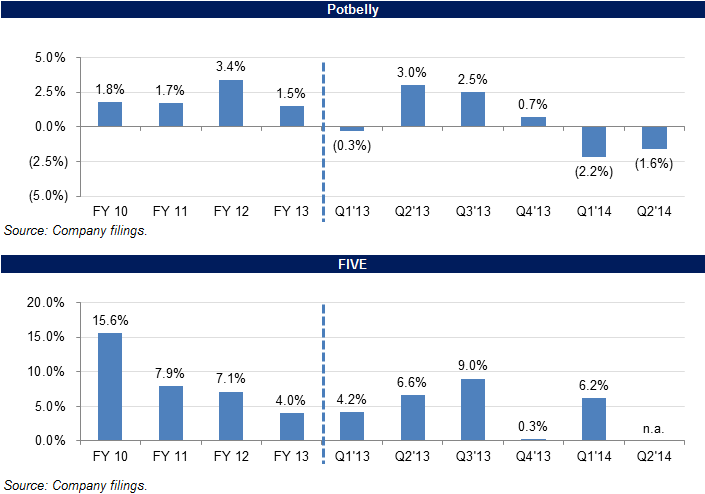

As we’ve highlighted in our previous articles on FIVE, we consider a decline in SSSG to be a key indicator of a loss of differentiation, encroachment from competitors and / or a change in consumer preferences. The troubles with TCS were evident several quarters ago as the company began to report declining SSSG. We see the same worrying trend with FIVE (note that FIVE generates the majority of its profits in the holiday season during Q4, so Q4 metrics are critical).

|

Historical Same-Store Sales Growth: TCS vs. FIVE |

|

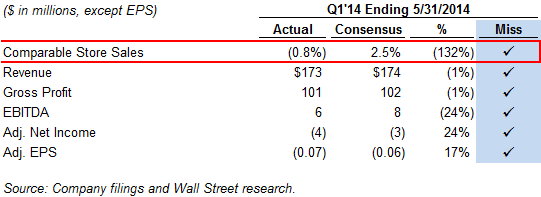

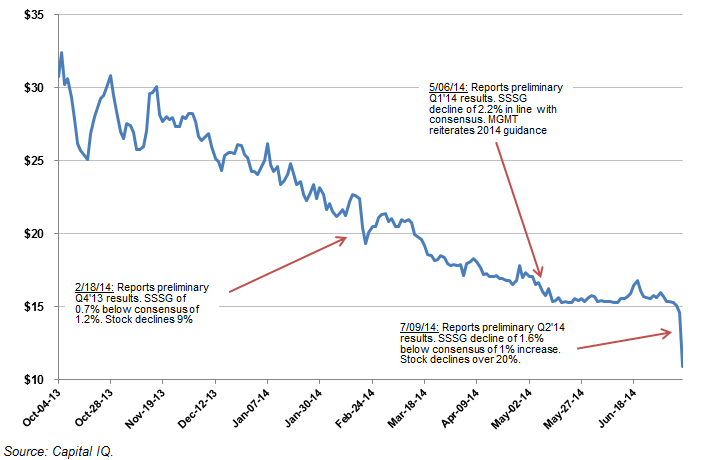

On July 8th, TCS announced earnings that missed analyst expectations, citing a tepid retail environment. Analysts were hoping for a sharp rebound in activity for the first quarter after a lackluster fourth quarter, but TCS missed Q1 estimates on all metrics, sending shares down by 15% in afterhours trading.

|

The Container Store: Q1’14 Earnings Highlight |

|

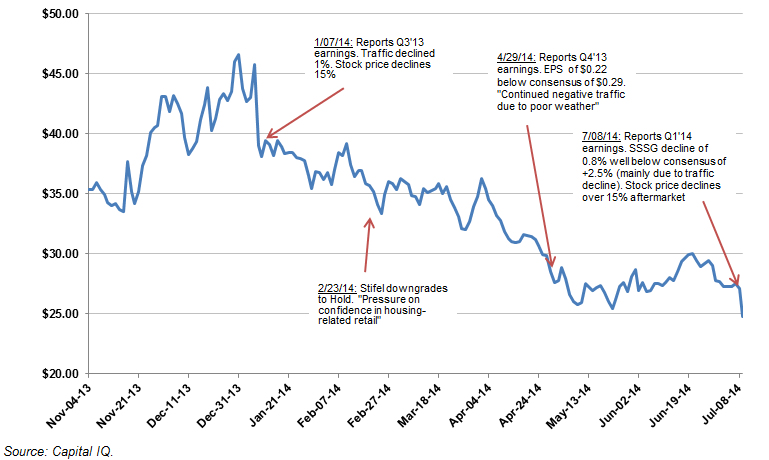

It should be noted that this is not the first time TCS has disappointed shareholders. This latest announcement follows poor earnings releases for the two previous quarters.

|

The Container Store: Recent Stock Price Performance |

|

While management attributed the poor SSSG in Q4’13 to poor weather (quote below), management blamed the weak Q1’14 on a “retail funk”:

“But now we’ve come to realize it’s more than just weather and calendar. Consistent with so many of our fellow retailers,we’re experiencing a — well, a retail funk. I mean, so many retailers that we talk to are experiencing that.”

– William Tindell (TCS CEO) on TCS Q1’14 Earnings Call

We don’t believe that “retail funk”, coming at a time when the U.S. economy is booming and the housing market remains healthy, is a one-time non-recurring phenomenon that indicates that poor operating performance will be short-lived. Rather, we believe that TCS is suffering from increased competition from other furniture retailers, and that customers are either demanding lower prices for its products and / or spending their container budgets elsewhere. TCS management admitted as much in their earnings conference call:

“We recognize that consumers have an inordinate appetite for promotional levels right now. And we recognize that this continues to be an incredibly promotional consumer environment.”

– William Tindell (TCS CEO) on TCS Q1’14 Earnings Call

The “promotional” environment that Tindell is citing is a permanent feature of furniture retailing; as long as retailers have sold storage boxes and containers, hundreds of competitors have vied to provide superior products at lower prices than their rivals. The Container Store sells storage solutions, shelving, hangers, drawers, and boxes. So does Bed, Bath & Beyond, Wal-Mart, Pottery Barn, Ikea, and hundreds of other competitors. To move inventory, these competitors often cut prices and offer sales, forcing The Container Store to either match their promotions, or to suffer “traffic declines”, a recent TCS operating trend that Tindell lamented five times in the most recent conference call.

If we were to cite just one reason why TCS is down 11% month-to-date, it would be that The Container Store simply does not have sufficient differentiation over competitors to justify a 20x EV/EBITDA and 2x EV/revenue multiple. We think the same is true for FIVE, whose EV/EBITDA and EV/revenue multiples are 3.5x and 26x, respectively.

Additionally, we think that one of the drivers behind TCS’s multiple compression has been a failure to meet the unit-growth expectations embedded in the company’s high valuation multiple. Last year, the company grew its store count by only 11%, and in 2014, TCS is projecting net new store growth of 10%. In the face of stiff competition, TCS has chosen to be more cautious about its store expansion program, cognizant that a misstep could have serious adverse long-term consequences for the company. FIVE has taken a different approach, attempting to grow store count by more than 20%+ in FY 2014, which equates to more than 60 new stores. We believe that the risk of execution mistakes is high for FIVE, and that in its attempt to meet lofty analyst expectations, the company may lock itself into onerous lease terms, disadvantageous locations, and spread its senior management too thin to achieve attractive operating metrics at its new locations. Alternatively, if FIVE backs away from its aggressive expansion plans, we may see the same multiple compression suffered by TCS.

PBPB Down 25% after Releasing Preliminary Q2’14 Results

As with TCS, PBPB has been another overhyped unit-growth story that has seen its valuation compress dramatically since its IPO. PBPB has shown generally anemic SSSG over the past few quarters, and last week many investors finally threw in the towel as the company’s same-store sales posted their second consecutive quarter showing a year-over-year decline.

|

Historical Same-Store Sales Growth: PBPB vs. FIVE |

|

On July 9, 2014, PBPB released preliminary results for the second quarter, warned of weaker-than-expected sales and lowered its outlook for the year, sending the shares down more than 20%.

Since its IPO, PBPB is down 54% and its valuation has declined from 2.9x EV/Revenue and 30x EV/EBITDA to 0.8x EV/Revenue and 8.1x EV/EBITDA. The severe valuation contraction again illustrates the vulnerability of specialty retailers and restaurants that fail to meet expectations from investors who demand flawless execution.

|

Potbelly Corp: Stock Price Performance Since IPO |

|

Similar to TCS’ recent earnings, the focal point of PBPB’s earnings miss was the SSSG decline of 0.8% (according to consensus estimates, analysts were expecting an increase of 1%). Like TCS, PBPB attributed the Q4’13 -Q1’14 SSSG decline to inclement weather but could not recycle that excuse for Q2’14.

“We are disappointed by our performance during the second quarter, which fell short of our expectations. Comparable store sales growth improved as we moved throughout the quarter, but fell short of anticipated levels. Given our results in the first half of the year, we have revised our full year guidance to reflect current trends within our business.”

– Aylwin Lewis, PBPB CEO on Preliminary Q2’14 Results

While Potbelly management hasn’t been very forthcoming about what has been hampering their same-store traffic, it may be continued competition from other sandwich shops like Jimmy Johns, Subway, Firehouse, Quiznos, etc, or a large number of maturing stores whose customers have diversified to other fast food options. Similarly, FIVE faces increasing competition from other dollar stores, Wal-Mart small format stores, potential copycats catering to the teen demographic, and a wide variety of other competitors within the discount retail sector. It also has an increasingly maturing store base that could begin posting dissappointing SSSG as stores reach peak operating metrics.

Like TCS, an overall lack of differentiation compared to competitors has prevented PBPB from driving sufficient traffic or enjoying sufficient pricing power to justify the company’s 30x+ EV/EBITDA multiple at the beginning of the year.

Conclusion

As we have illustrated in our past several articles, we believe that FIVE’s current valuation of 3.5x LTM Revenue, 26x LTM EBITDA and 52x P/E is overly optimistic. The recent valuation declines for TCS and PBPB highlight the dangers in underestimating the ferociously competitive nature of the specialty retail sector.

Similar to Five Below, TCS and PBPB were trading at extremely high valuations at the beginning of the year despite insufficiently differentiated business models, and shareholders have suffered steep losses as the companies have failed to meet the market’s lofty expectations. For its latest quarter, TCS missed EPS estimates by only one cent but the stock declined by 15%. For PBPB, SSSG improved in the latest quarter but failed to meet investors’ expectations, leading to a 20% stock price decline. These recent events underscore the risk that FIVE’s investors take when paying such a high valuation for an emerging retailer: any future misstep by FIVE could lead to a severe share price decline.

Add New Comment