Five Below, Inc. (FIVE) Part 3

New Morgan Stanley Initiation Relatively Lukewarm To FIVE's Valuation

Disclosure

We are short shares of FIVE. Please click here to read full disclosures.

Summary

- FIVE’s valuation multiples are higher than historical multiples of other successful concepts in their growth phases. We compare FIVE’s multiples to those of several brands highlighted by a sellside analyst

- Morgan Stanley’s initiating coverage report last week is relatively bearish. Given lack of secular growth drivers and valuation above high-growth peers, MS does not believe FIVE’s current valuation is compelling

- Teen retail faces numerous headwinds, with too many specialty retailers competing for teen discretionary spending. Many teen retailers are closing stores and trying to recover from SSS declines in 2013

- FIVE will face increasing threats from e-commerce. It has mistimed its plans to build a national brick-and-mortar business as the industry experiences a paradigm shift towards consumers shopping more online

Introduction

Over the past month, we published reports highlighting how Five Below (FIVE) is an overhyped retailer that’s unlikely to meet the lofty expectations baked into its inflated valuation multiples. In our first article, we showed how the company operates in a crowded and increasingly competitive sector where expansion by rivals will likely pressure margins, returns on capital and long-term growth rates. The company has been witnessing declining same-store sales growth, and margins currently stand at inflated levels relative to other dollar stores. When compared with other fast-growing retailers, FIVE’s valuation multiples stand out as outliers. In our second article, we highlighted how the specialty retail sector, as a whole, consistently disappoints investors due to unforeseen competition. We provided numerous examples of busted retail IPOs that failed to live up to their hype, and provided case studies illustrating how specialty retailers’ profits can be decimated quickly through competition. In this, our third article, we highlight further issues with FIVE’s valuation. Even if FIVE is able to achieve its growth plan, we believe the current valuation is so far above fair that investors are still likely to earn a sub-par return.

FIVE’s Valuation Is So High it Exceeds the High Growth-Stage Multiples of Even Extremely Successful Retailers

As we previously highlighted in our second article on FIVE, specialty retailers tend to have a typical lifecycle: when a concept is new, it achieves high same-store sales growth, high unit growth and expanding margins in the early years of its lifecycle. However, in specialty retail this period tends to last only a short while, and is generally followed by a contraction in revenue and margins in later years as competitors copy successful themes, execution becomes more difficult with a larger store base, and maturing stores begin showing pedestrian operating metrics. The probability that FIVE’s concept generates long-lasting, sustainable profits is incredibly low, no different than other case studies we highlighted such as Francesca’s, Tilly’s or Denninghouse. However, even if we assume that FIVE does become one of the small percentage of emerging concepts that transforms itself into a mature retailer with sustainable margins and growth rates, FIVE still appears overvalued when compared to historical players, and few successful retailers have ever traded at valuations as high as FIVE’s current levels at this point in their growth trajectories. For instance, let’s compare FIVE to several successful concepts cited by a bullish sellside analyst. In its initiating coverage report from February, Janney Capital wrote:

“Our fair value is $45/share, based on a 50x P/E multiple, and a 24x EV/EBITDA multiple on our 2014 estimates (FY15). Although the valuation is above its peers, this growth has proven worthy of this premium in the past, as we saw with fast growing companies like CAKE, PNRA, and PF Chang’s in the early 2000s, which traded at high multiples due to predictable growth despite more modest comp trends.” – Janney Capital 2/05/2014

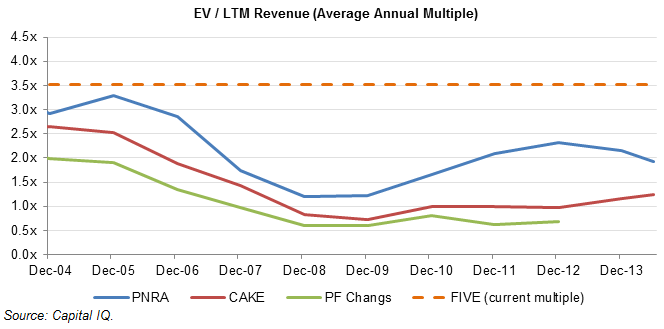

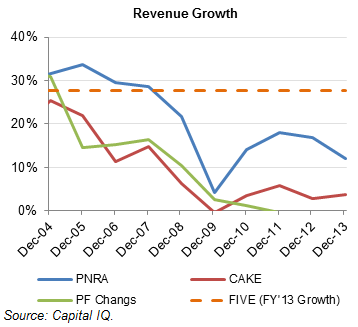

Below is a chart comparing FIVE’s current revenue multiple of 3.5x EV / LTM revenue to the revenue multiples of The Cheesecake Factory (CAKE), Panera Bread (PNRA) and P.F. Chang’s over the past 10 years. As shown below, FIVE trades at a revenue multiple substantially above any revenue multiple seen at those other successful concepts over the past ten years.

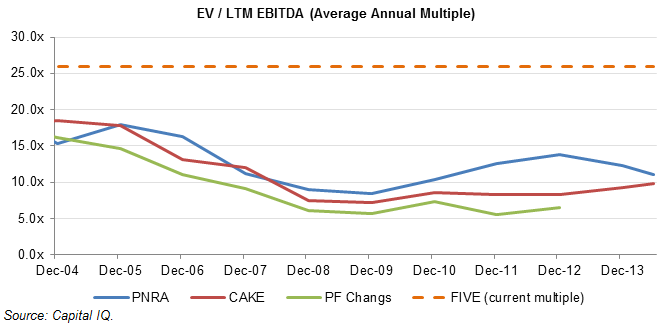

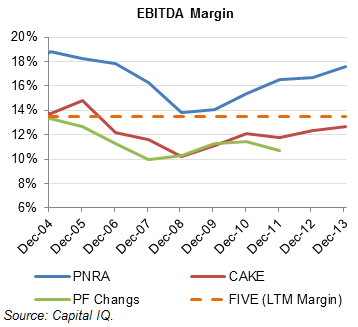

Next, let’s compare cash flow multiples of FIVE to PNRA, CAKE and P.F. Chang’s. Rather than using P/E multiples, which can be distorted by non-operating charges and variances in capital structures, we will compare EV / EBITDA multiples. FIVE’s current EV / EBITDA multiple is a staggering 35% higher than the highest multiple achieved by any of these comparables over the past 10 years.

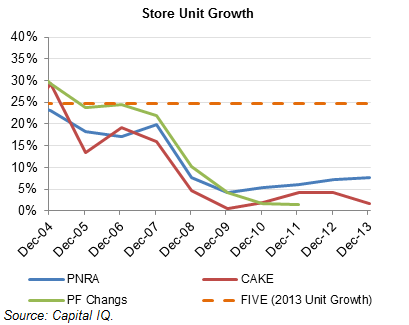

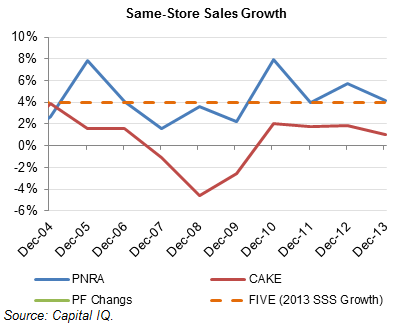

Yet despite trading at lower multiples over the past decade, these companies have achieved better or comparable unit growth, same store sales growth and profit margins. Below we compare FIVE to PNRA, CAKE and P.F. Chang’s on four metrics: unit growth, same-store sales growth, EBITDA margins and total revenue growth.

During the early years of our data set, we see comparable metrics amongst all the companies, yet materially lower multiples for PNRA, CAKE and P.F. Chang’s when compared to the current valuation multiple of FIVE.

|

Store Unit Growth (Y-o-Y) |

Same-Store Sales Growth (Y-o-Y) |

|

|

|

|

In later years, as these concepts matured, store unit growth declined and revenue growth slowed materially, leading to the eventual decline of valuation multiples. We expect to see a similar pattern for FIVE as it has already exhibited declining overall sales growth, same-store sales growth and store unit growth.

Additionally, we would note one important distinction between a discount retailer like FIVE, and fast-growing concepts like PNRA, CAKE and PF Chang’s; the comparables are food retailers, whereas FIVE is a discount retailer. Though the dining industry is incredibly competitive, restaurants can be significantly more differentiated than discount retailers. There is a discernible difference between eating a burrito at a Chipotle versus a Taco Bell, just as there is a discernible difference between eating at a Panera Bread as compared with the local deli.

However, in discount retail, the differences between competitors are much less, whether we’re comparing dollar stores like Dollar General and Family Dollar, or drugstores like Rite Aid and Duane Reade. Rather than relying on competitive advantages like trending products or better-tasting food, discount retailers typically compete on location and price, the latter of which is typically a function of scale advantages and being a lower cost operator. In this respect, a discount retailer like FIVE is more poorly positioned to expand nationally while maintaining 14% EBITDA margins and attractive same-store sales growth, as compared to PNRA, CAKE or PF Chang’s.

Since FIVE has limited sustainable advantage in cost (when compared to other dollar stores, for example) and merchandise (when compared to a Zara, for instance, which produces its own products), FIVE’s operations are more replicable than the restaurant chains we’ve been highlighting. In fact, as we discussed in our first article, Dollar General has already stated its intention to copy some of FIVE’s successful aspects, and FIVE’s same-store-sales growth has already begun to slow, and earlier in its lifecycle than the restaurant comps mentioned in the Janney report.

Recent Initiating Coverage Report by Morgan Stanley Relatively Bearish

Last week, Morgan Stanley (MS) launched coverage of FIVE with an equal-weight rating and $41.00 price target, and wrote a 20-page initiating report that elaborated on numerous obstacles FIVE will face as it tries to grow into its 50x+ LTM P/E multiple. Although Morgan Stanley’s official rating on FIVE is “equal-weight”, we interpreted the report to be relatively bearish on the company, given that sellside equity analysts rarely issue “Sell” ratings, especially in initiating coverage reports. Reading between the lines, we believe that Morgan Stanley agrees with us that FIVE’s valuation multiples are stretched and that there exists considerable potential downside for the stock. The main thrust of MS’s report is that although FIVE is growing nicely, its growth prospects are sufficiently reflected in the stock’s high valuation. In its introductory subheading, MS ends with “at 34x 2015e P/E and a PEG of 1.1x, we believe [the company’s growth] potential is largely priced in.” We believe MS expressed concerns on a number of fronts. With respect to the company’s fickle teen end-market, MS noted that if FIVE fails to spot a trend, the company’s results could suffer, which we’ve also previously highlighted. MS wrote that “if FIVE misses its second to market goal with a trend, sales could be lost.” Later in the report, continuing on the topic of management’s ability to remain on top of trends, MS wrote “there can be blips along the way, as evidenced by 4Q13 results which fell short of original guidance. Even during 3Q, which had comp upside, management noted that Black Friday fell short of its internal expectations.” MS also addressed the debate of whether FIVE’s product line is sufficiently differentiated. While it noted that FIVE has carved out a niche in catering to the teenage end market, “similar products are available at a variety of other outlets, including big box retailers, discounters, independents and online, amongst others.” Morgan Stanley also noted the weak consumer environment for teen-focused retailers, writing:

“Teen backdrop not ideal right now, though FIVE’s value focus is ‘in trend.’ We think FIVE caters to its demographic well, with its value-focused price points and creative product assortment. That said, should the macro backdrop for the segment worsen, we believe there could be a pull-back in sales given the discretionary nature of Five Below’s merchandise.” Source: Morgan Stanley, “High (Flying) Five – Initiating Equal-weight, $41 PT”, June 24 2014

Teen retailing has been a weak sector for quite some time now, and is certainly not a secular growth story within retail. We address the macro headwinds for teen retail later in this article.

Morgan Stanley discusses how the high expectations baked into the company’s valuation could result in substantial downside volatility in response to adverse events. For instance, when FIVE lowered guidance in January 2014, the stock declined 13% on that day, highlighting the sharp losses FIVE investors can suffer when FIVE shows signs that it may not meet the market’s lofty growth forecasts.

“High growth nature = high expectations = good chance for volatility. Exemplified by its already premium multiple, we think the high growth nature of FIVE demonstrates that investors’ expectations for the company are also high. As such, we do think there is a good chance for volatility around data points, either positively or negatively…. As referenced above, in relation to the company’s recent 4Q results, the stock reacted negatively following FIVE’s lowered guidance in January 2014. The company guided 4Q results down to a negative comp, which would have been Five Below’s first as a public company. Ultimately the company posted a +0.3% comp for the quarter. While results were ahead of lowered expectations, we note that earnings were still well below original guidance.” Source: Morgan Stanley, “High (Flying) Five – Initiating Equal-weight, $41 PT”, June 24 2014

Like us, Morgan Stanley appears concerned that FIVE’s valuation is simply too high, despite the company’s operating momentum. Under the heading “Growth potential appears priced in at current valuation”, MS writes “at 34x [forward] P/E versus a post-IPO average of 43x and a PEG of 1.1x, we believe [the company’s growth] potential is largely priced in.”

Morgan Stanley ends its report with a relatively bearish statement, when viewed in the context of the typically rose-colored glasses of a sellside analyst:

“Given the lack of secular growth drivers and a valuation above the high-growth peer average, we do not believe current valuation is compelling for FIVE.”

Teen Retailing Backdrop Unhealthy

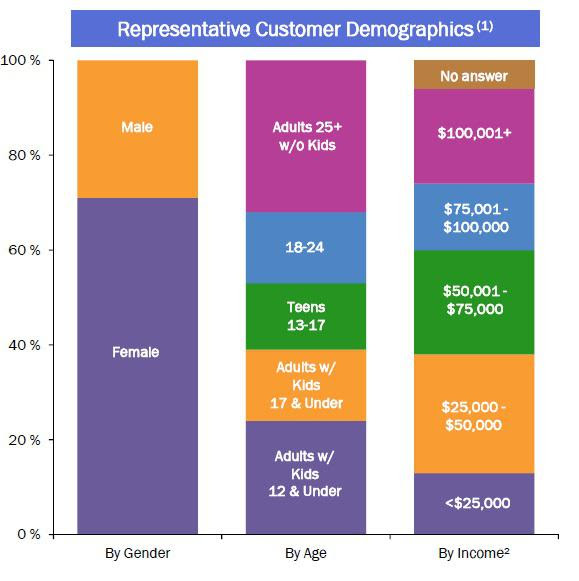

One of the headwinds facing Five Below is that its key end market, teenagers, remains among the weakest demographics in retail. As we can see below, more than 50% of the company’s customers are teens, pre-teens and their parents:

Source: Company Presentation

Teen retail has been facing significant secular challenges. For instance, in its June 3rd report “Apparel Retail – The Mall Manual / June Edition: Teen Retail Down and Out… But Probably Not Forever”, RBC wrote:

“Forgive us for stating the obvious but the teen space has likely been the most difficult and challenged sub-sector of apparel over the last year and a half. Teen retail is not alone in its underperformance, as the softlines sector overall has struggled, but it has clearly been hit hardest.” Source: RBC Securities, “Teen Retail Down and Out… But Probably Not Forever”, June 3 2014

In its review of first quarter results for teen retailing, entitled “Retailing/Specialty Stores: Smells Like Teen Spirit… What We Learned From 1Q Reporting”, Jefferies also highlighted the sector’s negative trends. Its first two points in the report’s “10 Key Takeaways from 1Q Reporting” were:

1) It’s Not Pretty Out There… 1Q results were tough with sales subdued and gross margins compressing further as mall traffic was weak and promotions were high, though much of this was to be expected.

2) 2Q Outlooks Not Good… Coming into 2014, we had initially thought that 1Q would mark a trough in teen sector fundamentals. This proved not to be the case, as 2Q guidance was fairly downbeat. Jefferies, “Retailing/Specialty Stores: Smells Like Teen Spirit… What We Learned From 1Q Reporting”, June 3 2014

Jefferies further discussed how teen retailers are closing stores at a breakneck pace, writing:

“Store Closures Mounting… Teen retailers are projecting even greater numbers of store closures, which will help balance supply with reduced (and soon stabilizing) demand. We continue to believe 30% of store supply could come out of the teen retail market over the next 3 years.”

While FIVE is rapidly expanding its unit count, other retailers that cater to the teen demographic are shrinking their store base. Abercrombie (ANF) has announced plans to close 60-70 stores in 2014, Aeropostale (ARO) has identified at least 175 stores to close, and Wet Seal (WTSL) has announced plans to close 14-18 stores upon lease expiration. Other teen retailers like Urban Outfitters (URBN) have slowed store growth dramatically, with URBN’s 2013 square footage growth only amounting to 6%, as compared to 15% to 20% between 2005 to 2007, and 8% to 10% in 2011-2012. The adverse trends within teen retail can be seen in the same-store sales declines of some of the largest publicly traded teen-focused specialty retailers. Below is an analysis by KeyBanc:

The same-store sales reversals range from a 3% decline at Buckle (BKE) in the holiday quarter of fiscal year 2013 to 15% declines at WTSL and ARO.

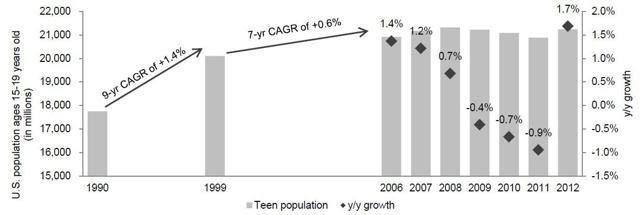

The causes of the teen retail downturn have been numerous, including competitive threats from e-commerce, persistently high teen unemployment, and an oversaturated sector replete with simply too many specialty retailers vying for teen discretionary spending. To make matters worse, KeyBanc also notes that overall teen population growth has been stagnant in the United States:

“The teen population has seen little growth in the last 10+ years. While the number of teen retail stores has significantly expanded, the actual teen population (U.S. population between 15-19 years old) has been relatively stagnant. From 1990-2012, the teen population grew at an annual rate of +0.8%, and only 0.4% from 2005-2012, well below the 5.2% annual adjusted square footage growth in the teen space.”

KeyBanc, “Overstored Teen Retailing: Softlines and REIT Perspectives”, March 19 2014

Source: KeyBanc, U.S. Census Bureau

Source: KeyBanc, U.S. Census Bureau

The competitive pressures within the teen retail sector present obstacles to FIVE, whose stores cater to teenagers and their parents, as it attempts to grow rapidly enough to justify 50x P/E and 3.5x EV / revenue valuation multiples.

Brick-and-Mortar to Online: A Paradigm Shift

“And I think this part of my remarks are very important. Over the last month or so, I’ve heard many traditional brick-and-mortar retailers attribute the downturn in their core business during holidays to factors such as a shortened holiday shopping season, a weakened consumer, the U.S. government shutdown… Respectfully, those explanations ignore a larger fundamental truth. And that truth is that traditional brick-and-mortar retailing is at an inflection point. No longer are many retailers only required to compete with stores on the other side of the street. They are now required to compete with stores on the other side of the country. Navigating this seismic shift will continue to be very, very difficult for many.”

– Howard D. Schultz, Founder, Chairman and CEO of Starbucks Corp. on 01/23/2014 Earnings Call

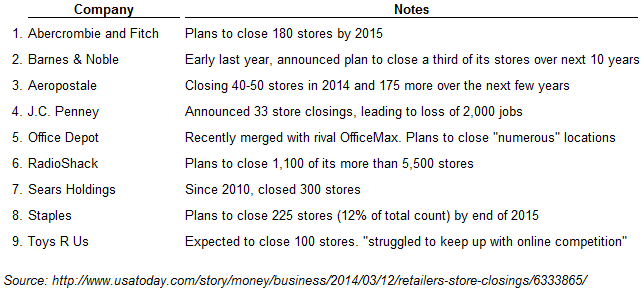

Over the past few years, we’ve seen retailers from Staples to Abercrombie

|

Nine Retailers Closing the Most Stores |

|

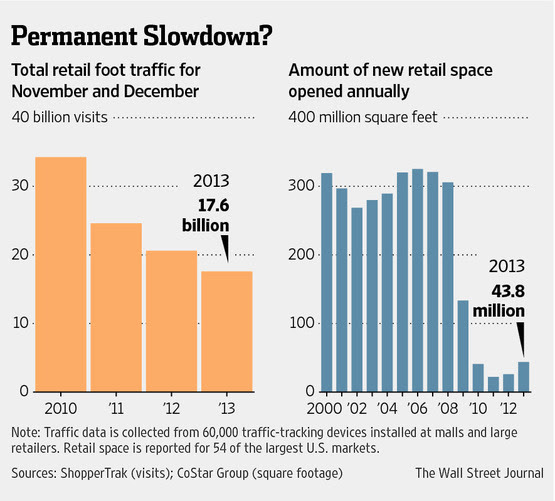

According to this WSJ article, e-commerce has resulted not only in reduced retail foot traffic, but also in less and less new retail space opened annually. Given these facts coupled with the numerous store closings by some of the nation’s largest retailers, we believe that FIVE underestimates the growing e-commerce threat.

|

Decline of Retail Foot Traffic and New Retail Space Opened Annually |

|

While FIVE could launch its own e-commerce platform, the management team does not seem to be focused on that front. On its latest earnings call, the CEO largely ignored an analyst’s question about its digital strategy.

The other piece is what does a company at some point do with somewhat of an online strategy, which is a great question, but is one really that I don’t think we are prepared to discuss today, while it may be a great opportunity at some point. – Thomas Vellios, CEO of FIVE on Q1’14 earnings call on 6/04/2014

Overall, we believe that FIVE’s plan to grow as a B&M retailer is poorly timed. We expect margins and growth to come under pressure as even larger and more established retailers have succumbed to the e-commerce threat.

Conclusion

As we have highlighted in our past three articles, we believe FIVE is a grossly overvalued retailer with limited sustainable advantages and pricing power. It operates in a sector catering to a struggling consumer demographic, teenagers. While other teen retailers are reducing store counts and square footage, FIVE is rapidly expanding. At the same time, FIVE’s overall industry, brick-and-mortar retailing, is facing competitive pressures from Amazon and other forms of e-commerce, which is decimating industry stalwarts like Office Depot (ODP) and Staple’s (SPLS). Yet FIVE continues to rapidly expand, increasing its store count at a 20%+ clip. Despite industry headwinds, FIVE trades at valuation multiples that even the few specialty retailers that have been able to expand nationally rarely or never traded at. It’s no surprise to us, then, that the most recent sellside analyst to launch coverage on the company gave FIVE a relatively lukewarm review, citing that the current valuation is not “compelling”. Not only do we deem FIVE’s 50x+ LTM P/E and 3.5x EV/revenue multiple less than compelling, but we think that the stock is an attractive short and will likely disappoint long investors who are ascribing growth rates too lofty for the company to achieve.

Add New Comment