Disclosure

We are short shares of MLNX. Please click here to read full disclosures.

We believe that shares of Mellanox Technologies, Ltd. (MLNX) are highly overvalued, not only because it is a semiconductor company operating in a small and technologically fast-changing niche trading at an absurdly high valuation, but, equally as important, the Intel CPU chip upgrade cycle which fueled its past few quarters of atypical growth is about to plateau, and then sharply decline.

We are short and own put options on shares of MLNX.

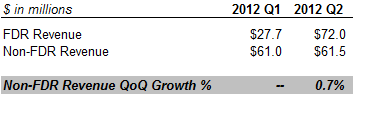

Investors apparently misunderstand the cyclical nature of Mellanox’s 56 GB/s “FDR” Infiniband business and have mistakenly extrapolated the recent uptick in Q1/Q2 growth into a long-term trend. As the upgrade cycle for Intel’s Romley CPU plays out, Mellanox’s FDR revenue could plateau in Q4 2012 and sharply reverse in 2013. When this occurs, the 50%+ quarter-over-quarter growth that investors have come to expect will be a thing of the past. As Mellanox’s lead product (54% of Q2 2012 revenue), FDR has been tailored specially for the Romley CPU system, meaning that FDR revenues probably tie very closely to Romley CPU shipments. Using this assumption and FDR revenue estimates, we estimate that quarter-on-quarter growth of the base business, excluding FDR-related revenue, was only 0.7% in Q2 2012. Non-existent growth in the core business hardly justifies the 50% share price bounce (from $65 to $95) that Mellanox experienced after its second quarter earnings release, let alone the further increase to $110 in the past two months.

Unfortunately for most investors, the cyclical nature of the tech hardware business is rarely modeled by analysts, who prefer straight-line forecasts and sky-high, AMZN-like valuation multiples for whichever business is in vogue at the time. But while they lavish Mellanox with unbounded praise in their qualitative analysis, most analysts have actually modeled a material growth slowdown in 2013. As such, we believe that investors in MLNX are currently playing with fire and would be wise to avoid shares at the current astronomical valuation level.

As for the notion that MLNX may be acquired, the idea of an acquisition is preposterous at prices anywhere close to the current trading levels. A scan of the tech landscape tells us that of the few strategic buyers that might exist, most couldn’t afford MLNX’s current valuation (such as ELX, QLGC, HPQ). Those that can would prefer higher-margin branded products and services (ORCL and IBM), or have already made their Infiniband investments (INTC). Others would likely allocate internal resources to create a next-generation rival product instead of overpaying for a risky acquisition (BCOM). Since Infiniband remains a small niche market confined to high-end supercomputing, no rational buyer would consider acquiring MLNX for a $5+ billion valuation, in our opinion.

Notwithstanding its current share price bubble, we believe that Mellanox has built itself a niche business and achieved a big win through the Romley upgrade cycle. But high-speed computing is a cutthroat space and Mellanox still faces competitive risks from all sides (e.g. Intel’s Infiniband and Cray interconnect, 40GB/s low-latency Ethernet, etc.). Since high-tech hardware is such a cyclical, competitive space, almost all peer companies trade below 10x Forward EV/EBITDA and many trade below 5x. Mellanox’s 28x FY12E EBITDA is in another stratosphere, and as frequently occurs in the tech space, we expect shares to sharply snap back at the slightest earnings waver. Make no mistake about it: this is a momentum-driven growth stock and its shares can only levitate at these prices while the company delivers spectacular growth numbers. Even Mellanox can only defy gravity for so long.

The Romley Upgrade Cycle Has Driven Short-Term Growth

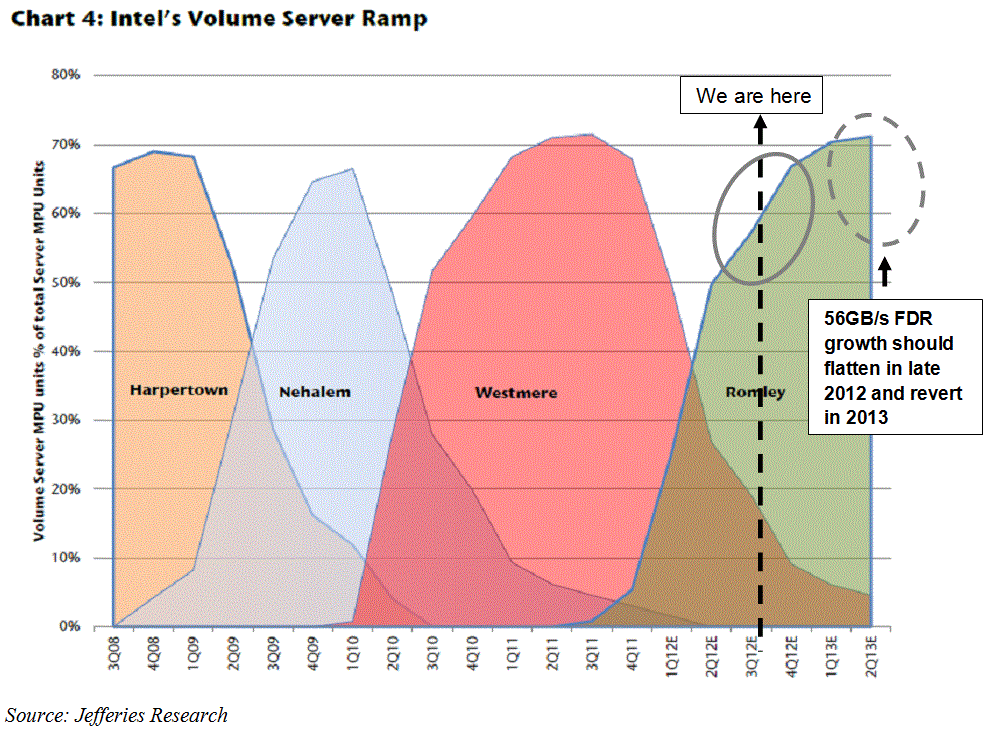

Mellanox provides premium Infiniband chips used in high-performance computer (“HPC”) clusters. Infiniband is a hardware interconnection tool that allows stacks of databases, servers, and computers to ‘talk’ to one another. While most commercial servers are perfectly content with 1G/s or 10G/s Ethernet interconnection, a small niche of specialized HPC clusters prefer the higher speed and low latency of Infiniband, of which MLNX is the leading supplier, and are willing to pay the higher prices associated with it. In particular, Intel’s Romley CPU core, which was released in 1Q 2012, included Mellanox’s products as among its preferred interconnection tools; therefore, as has been the case over the last few quarters, each time that an HPC cluster upgrades to the Romley core, many will purchase the FDR interconnectors as well.

We believe that investors do not fully appreciate the cyclicality of Mellanox’s business. Intel’s supercomputer processing units, the industry standard, undergo predictable product cycles. Sales will ramp for three to four quarters before plateauing for a quarter or two. CPU motherboard sales then fall sharply ahead of a new product launch since customers won’t pay top-dollar for soon-to-be outdated technology. Because Mellanox’s FDR Infiniband chips are usually purchased alongside high-end CPUs, Mellanox’s sales cycle should track closely to the Romley cycle. In fact, since much of Mellanox’s FDR customers represent the highest-end of the supercomputing market, we would actually expect the FDR cycle to have a shorter duration than the overall Romley cycle. This is because those willing to pay the extra costs for FDR over Ethernet were probably also the first in line for the upgrade in Q1 and Q2 2012. Therefore, we expect that Mellanox’s temporary Romley-related uplift will be gone by Q4 2012 or Q1 2013, potentially eliminating up to half of Mellanox’s revenuein the quarters ahead of the next server CPU launch. Since most analysts have merely assumed straight-line quarter-over-quarter growth, we believe that Mellanox could materially miss estimates during Q4 2012 or FY 2013 earnings reports.

Below is a chart of Intel’s Romley server upgrade trajectory, as compared with historical high-end HPC server cycles.

(click to enlarge)

As we can see, the Romley server ramp will probably plateau within the next few quarters. Then Romley purchases should plummet.

The most recent 10Q discloses FDR-related and non-FDR-related revenue in Q1 2012 and Q2 2012. Growth in non-FDR related revenue was essentially flat in Q2 2012 compared to Q1. As previously discussed, a majority of FDR revenue is tied to the Romley CPU system.

Deutsche Bank acknowledges the impact of the Romley release by stating, “Anticipation of the Romley release led to some pent-up demand for Mellanox’s products, which at least partly explains the 111% YoY increase in revenues in Q2 2012” (DB September 4th, 2012 Research Report). Even more worryingly for Mellanox, Intel has indicated that Romley uptake may have spiked more quickly than previous cycles. INTC stated that “one month after launch, Romley has shipped nearly twice the volume of Nehalem at the same point in its ramp” (Q1 2012 Earnings Call).

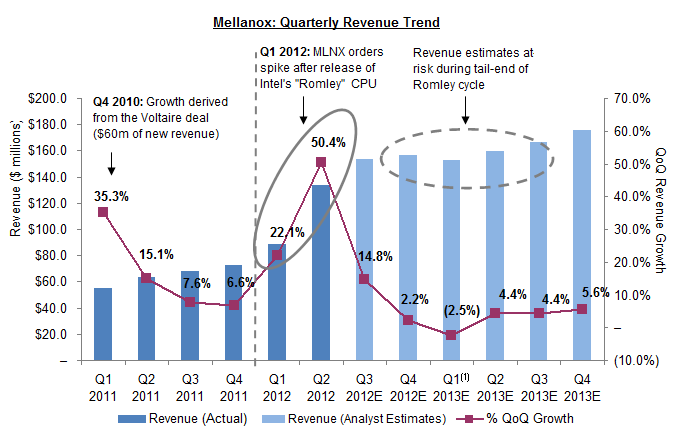

The chart below shows revenue estimates using Wall Street consensus. We’ve also overlaid grey circles to represent how we expect the Romley product cycle to play out. Notice that analysts only have a 3% slowdown forecasted for Q1 2013. Compare that to the expected Romley product cycle in our graph above and you have the recipe for a big earnings miss.

(click to enlarge)

Sources: CapitalIQ, Bloomberg, Company filings

(1) The number of available estimates for Q1 2013 and onwards decreased from twelve to nine.

Despite their flourishing compliments and extraordinary target prices, Wall Street analysts generally agree that the recent uptick in revenue growth cannot be sustained. Analysts expect MLNX to revert to single-digit top-line growth by Q4 2012. This type of growth profile hardly justifies Mellanox’s current 9.0x 2012E revenue (26.7x EBITDA) valuation multiple. For comparative purposes, Facebook has a 6.3x 2012E revenue multiple, Apple is about 3.5x, and Broadcom is 2.4x.

Tellingly, Mellanox management only offers guidance for one quarter out (Q3 revenue guidance of $150-$155m). Perhaps this is because they don’t want to alert the Street to a potential contraction as the Romley cycle ebbs. Here is an excerpt from the Q2 2012 Earnings Call:

<Equity Analyst>: “As we think about our models for December then, the December quarter, should we think in terms of there having been a lot of one-time business in the September quarter or should we think about growth again sequentially in the December quarter?”

<Eyal Waldman, Mellanox CEO>: “Sure. So, we can’t give you any guidance for the December quarter.”

It’s unusual for companies to provide guidance only one quarter ahead, and comments such as this indicate that management is in no hurry to open the kimono.

Very Few Businesses Actually Require 56 GB/S Speed

When it comes to purchasing CPU server processors, IT purchasing managers are practical. The vast majority of corporations are more than satisfied with less-costly 10GB/s Ethernet. Plenty of data centers even run at speeds of 1GB/s without any disruptions.

As such, the type of customer that is willing to spend hundreds of thousands, or even millions, of dollars to upgrade their server clusters every 2-3 years is few and far between. The high-end of the supercomputing market might include high-frequency trading, military applications, cutting edge physics and some web 2.0 / cloud computing companies, but most clusters don’t need ultra-fast low-latency performance. While we acknowledge that the overall high-performance computing market is expanding (7.5%/year according to the HPC Advisory Council), this is an ongoing secular shift rather than a sudden step-change, as the precipitous shift in Mellanox’s valuation would indicate.

40GB/S Low-Latency Ethernet: “Not as Far Away as You Might Think”

As we’ve previously alluded to, Ethernet is significantly cheaper than Infiniband. According to HP’s website, a 40GB/s Infiniband adaptor costs $1,295 while a 10GB/s Ethernet adaptor costs $699 and a 1GB/s Ethernet adaptor will run you only $229. That price differential is especially significant considering that a standard HP ProLiant server starts at only $858. Given this context, we believe that only deep-pocketed, price insensitive customers are willing to pay for Infiniband over Ethernet. That may soon change should 40GB/s Ethernet networks become widely deployed, causing some high-performance computing customers to switch to Ethernet. But Ethernet networks typically have higher-latency than Infiniband, latency being the other measure of speed along with bandwidth. However, if 40GB/s low-latency Ethernet networks become widely deployed, that could result in even more HPC customers might switch from Infiniband. On their August 9th Q4 2012 earnings call, Emulex, a maker of fiber channel and Ethernet connectors, announced its intention to create low-latency 40GB/s and 100GB/s Ethernet products:

“Customers have asked us to provide a low-cost alternative to InfiniBand that could be used to converge LANs, SANs and HPC workloads while allowing IT managers to leverage a common set of tools and practices in the data center. We see the opportunity to drive the second major phase of network convergence by combining HPC and IP networks on a single wire with software designed networking tools leveraging low latency 40gb Ethernet… Our investment in high-speed 40gb and 100gb Ethernet ASICs… will allow us to very effectively tap into the rapidly growing high performance computing opportunity. This strategy isn’t just about pointing into the future as we’re starting to make announcements in this space now.”

– Emulex President and COO, Q4 2012 Call

Emulex goes on to mention that they’ve had numerous customers in the “web and cloud space” inquire about an alternative to native Infiniband, which is costly and cumbersome. They also note that, “We’re not seeing InfiniBand so much in the storage space,” which Mellanox claims is roughly one third of their total addressable market (3.4m of 11.8m endpoints).

Emulex currently trades below 1x 2012E revenue and around 4x EBITDA, which doesn’t bode well for MLNX’s future valuation should 40GB/s Ethernet displace a portion of Infiniband’s market share.

Is Infiniband Even the HPC Interconnect Technology of the Future?

Semiconductors are a very fickle business. Brief product life cycles exist thanks to the continued proof of Moore’s Law. This year’s hero could be the next year’s zero. At the moment, Mellanox is only one of two suppliers that make silicon for InfiniBand switches and adaptors, the other being QLogic’s former Infiniband business. QLogic has historically lagged behind Mellanox’s technology, and thus decided to sell its InfiniBand business to Intel for $125m in January 2012. Intel was one of the original developers of Infiniband silicon in the early 2000s, but it then switched its focus to Ethernet technologies. QLogic’s Infiniband can only achieve 40GB/s, putting them a cycle behind on the technology curve. But many analysts believe that Intel’s next CPU core (i.e. Romley’s successor) may be able to bundle its in-house InfiniBand interconnection technology with its next generation server CPUs. Should this occur, high-performance computing clusters would have little reason to purchase high-priced interconnectors from Mellanox during the next product life cycle.

Additionally, if lower-cost Ethernet can be created to run at around low latency 40GB/s, many cost-conscious datacenters could efficiently operate without a proprietary Infiniband network. For an enterprise surrounded by such near-term technological risks, Mellanox currently trades at a completely unjustifiable multiple. That’s especially the case given that once the Romley CPU upgrade cycle abates, we expect Mellanox’s growth to materially slow over the next few quarters. Once the market foresees this, Mellanox’s astronomical valuation multiples will quickly fall back to Earth.

Highly Inflated Valuation is Unjustified

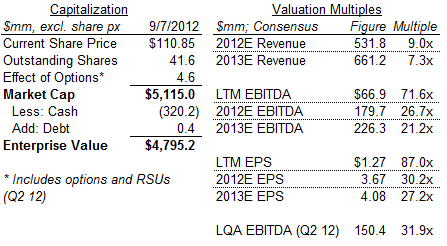

Below is a summary of MLNX’s valuation:

We would propose a thought exercise to any investor. Go ahead and check the valuation multiples for your current investments through Yahoo Finance, Bloomberg or a similar portal. We would guess that most are priced well below MLNX. As the Facebook IPO demonstrated, even disruptive monopolistic businesses are not good investments at inflated valuations, let alone single-product technological components suppliers.

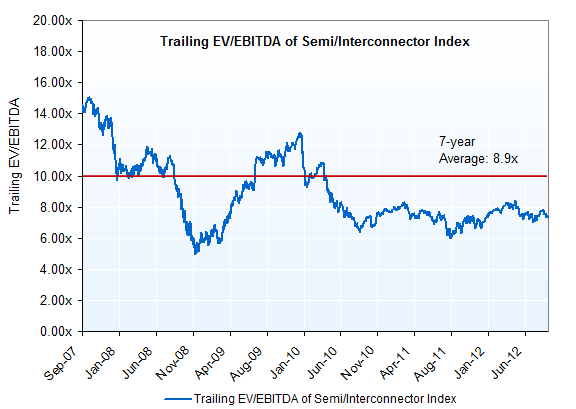

For additional perspective, we’ve indexed the historical trailing EV/EBITDA multiple for an index of semiconductor and interconnector companies:

As the chart below shows, the industry generally has traded well below 10x trailing EV/EBITDA for the past 2 years:

(click to enlarge)

Index includes Intel, Broadcom, QLogic, Emulex, Qualcomm, Texas Instruments, Broadcom, Microchip Technology, Marvel Technology, Brocade, ON Semiconductor, and Advanced Micro Devices

Source: CapitalIQ

Mellanox currently trades at 71x LTM EBITDA and 26x FY12E EBITDA, both well outside the range of our chart.

A Sober Analysis: What’s it Worth?

According to the industry-sponsored mouthpiece, the HPC Advisory Council, annual HPC interconnect revenue will reach $2bn by 2014. This trade group forecasts that Infiniband will have 43% of this market (vs. Ethernet and proprietary interconnectors).

While the industry analysts that we’ve spoken to believe that the $2bn market figure might be too high, we’ll be generous and use that figure to create an ‘everything-goes-right’ peak valuation target for Mellanox. Assigning Infiniband a 45% market share, in line with HPC’s estimate, would infer overall Infiniband revenue of $900m/year by 2014. If Mellanox dominates the market with 90% share, MLNX could theoretically achieve about $200m of revenue and $60m EBITDA per quarter, or $240m of 2014 EBITDA (using a charitable 30% EBITDA margin). Since this is a peak EBITDA target two years forward, we would generally assign a multiple below the industry peer average of 9x. But even if we use a princely 10-12x 2014E EBITDA multiple range, which is beyond the top-end of the industry’s trading range, the business would only be worth $2.7-3.0bn or $60-$70/share. This is not our estimate of the fair value. Rather, it is the highest valuation we could reasonably fathom should Mellanox execute perfectly over the next two years. This would not only be a herculean task in and of itself; it would require Intel to fail to generate its own Infiniband alternative to MLNX’s technology and would also require Infiniband to maintain its current market share relative to other technologies. We don’t see how a rational investor could possibly accept the risk-reward trade-off of MLNX’s current share price of $110 in light of these significant downsides.

Mellanox’s Valuation Appears Unsustainable Relative to Selected Peers

Below is a table comparing Mellanox’s valuation to other comparable companies in the Ethernet and Fibre Channel semiconductor sub-sector, as well as the general semiconductor sector.

(click to enlarge)

We think the best long-term comparables for Mellanox are the Ethernet/Fibre channel companies, Emulex and QLogic. Infiniband is currently experiencing a resurgence much like Ethernet did from 2006-2009. We can use historical valuations from that period to give us a sneak-peak into what the future might hold for Mellanox. The forward EBITDA multiples for ELX and QLGC briefly hovered near 10x in 2007 before reverting to the 5x – 8x range following the financial crisis. Based on this analysis and the trading range of our comparable index, we are comfortable assigning Mellanox a 10-12x FY14E EBITDA multiple, which we feel more than compensates Mellanox for its current technological lead. The prudent investor would of course only purchase or hold shares at a substantial discount to our ‘peak value’ case of $60-70/share.

(click to enlarge)

We believe that Mellanox’s valuation multiple will revert to levels much closer to its peer group once investors realize that Infiniband is susceptible to technological risks just like Ethernet was a few years ago and fibre networks were before that.

We’ve Seen This Movie Before…

The tendency for investors to mistakenly over-extrapolate a few quarters of growth is a recurring theme in the tech hardware industry. We would direct investors to study the share price corrections of Sycamore in 1999-2000 (optical switches for fiber networks), STEC in 2009 (solid state drives), or Acme Packet in 2011 (session boarder controllers for 4G-LTE). Time and time again, the market shows a tendency to project recent quarterly growth into a long-term trend. But frequently, growth will ebb following a short-term earnings spike as the product cycle peaks, new entrants emerge and the technological landscape shifts. The key for a rational investor is to understand why the market’s mispricing exists and compare that to historical precedents.

MLNX shares nearly tripled from $35 to $90 following the Q1 and Q2 earnings reports, reports we believe were driven to the upside by a short-term Romley upgrade cycle. MLNX’s stock was then boosted from $90 to $110 on July rumors of a buy-out by Oracle or IBM. Never mind that Oracle and IBM are extremely unlikely to pay $5bn+ for an inconsequential supplier (MLNX sales to Oracle were $18.3m in 2011). But fanciful rumors such as these are taken as legitimate news stories during investment frenzies.

What we view as more revealing than these press releases is the fact that MLNX conducted a secondary offering in late 2011 at prices 70% lower than current levels.

If Mellanox is Undervalued at $110/Share, Why was the Company Selling Shares at $31.75

On September 20th, 2011, MLNX diluted shareholders by about 10% by issuing 3m shares (plus a 450k greenshoe) at $31.75, netting MLNX $90.7m in gross proceeds. The Company did not disclose a specific use of proceeds, instead using boilerplate ‘general corporate purposes’ language. Since the Company had $102m of cash at the time and was cash flow positive, MLNX does not appear to have had a good reason for diluting shareholders. It is telling when a debt-free, cash flow positive business dilutes existing shareholders by nearly 10%. Perhaps management decided to take advantage of what it considered to be a frothy valuation at $31.75/share. Today, at prices 3.5 times higher than the September 2011 valuation, MLNX’s share price is no longer frothy; it is downright silly.

The 800 Pound Gorilla: Intel

“The markets in which we operate are extremely competitive and are characterized by rapid technological change, continuously evolving customer requirements and fluctuating average selling prices. We may not be able to compete successfully against current or potential competitors.”

– MLNX 2011 Annual Report

As Seeking Alpha contributor “Infitialis” adeptly summarized in his report, Intel has recently positioned itself to re-enter the interconnector market with three acquisitions in the past thirteen months: QLogic’s Infiniband, Cray’s proprietary interconnectors, and Fulcrum Microsystem’s Ethernet. We believe that this holistic approach to interconnector technology (i.e. more than just Infiniband) could allow Intel to offer a bundled CPU+interconnector offering when the successor to Romley is released.

At the moment, Intel appears to have made a strategic decision to delay direct competition with Mellanox during the Romley release. Instead, Intel is probably attempting to skip a product cycle and leapfrog Mellanox with a bundled offering. We believe that this week’s Intel Developer Forum might provide a glimpse into Intel’s interconnector future. At the current price levels, we believe MLNX shares could sell off sharply should Intel make any interconnector-related announcements.

The Intel Developer Forum

Much like the Apple product forums made infamous by Steve Jobs, Intel hosts a biannual Intel Developer Forum (IDF) to discuss its latest technological advances and product updates. The next IDF will be held September 11 – 13th and key items on the agenda include next-generation CPUs, smartphone/tablet processors, and Windows 8 integration. But what intrigues us with respect to Mellanox is Intel’s scheduled presentation dedicated to interconnector technology entitled, “HPC Fabric Performance Overview.” According to the agenda, “This session covers the architecture of the recently acquired Intel True Scale Fabric [QLogic’s Infiniband].” We would not be surprised to hear Intel hint at its next-generation interconnector technology, be it Infiniband or a Cray-related proprietary mode. If Intel can bundle its next-generation CPU with in-house interconnector adaptors and switches, Mellanox could lose most of its FDR-related revenues in 2014 when the successor to Romley is launched.

We’ll end this section with a quote from Scott Fulton, a journalist for the cloud computing website ReadWriteWeb, who remarked, “If anyone can compete with Mellanox using a QLogic product line, it’s Intel.”

Closing Remarks

In summary, we congratulate Mellanox for creating an exciting technology and building an impressive customer base. But the high-technology semiconductor business is extremely cyclical and the “alliances” developed with the OEMs during Mellanox’s temporary technological lead will count for little as competitors emerge. Low-cost, low-latency Ethernet or a bundled Intel CPU+Infiniband motherboard could very well disrupt Mellanox’s near-monopoly within the next few years. Even more ominously for investors, the recent surge in quarterly revenue growth is probably a fleeting event. Once the Romley upgrade cycle plays out, Mellanox’s FDR chip sales (54% of total revenue in Q2) should sharply reverse. If this causes an earnings miss in Q4 2012 or early 2013, MLNX’s share price should quickly correct itself far lower than today’s $110 trading level.

DISCLOSURE

WE ARE SHORT AND OWN OPTIONS ON MLNX AND STAND TO PROFIT FROM A DECLINE IN THE STOCK PRICE. WE MAY TRANSACT IN MLNX SECURITIES SUBSEQUENT TO THIS EMAIL. THIS COMMUNICATION IS FOR INFORMATIONAL AND EDUCATIONAL PURPOSES ONLY AND SHALL NOT BE CONSTRUED TO CONSTITUTE INVESTMENT ADVICE. NOTHING CONTAINED HEREIN SHALL CONSTITUTE A SOLICITATION, RECOMMENDATION OR ENDORSEMENT TO BUY OR SELL ANY SECURITY OR OTHER FINANCIAL INSTRUMENT OR TO BUY ANY INTERESTS IN ANY INVESTMENT FUNDS OR OTHER ACCOUNTS. THE AUTHOR HAS NO OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN AND MAY MAKE INVESTMENT DECISIONS THAT ARE INCONSISTENT WITH THE VIEWS EXPRESSED IN THIS COMMUNICATION. THE AUTHOR MAKES NO REPRESENTATIONS OR WARRANTIES AS TO THE ACCURACY, COMPLETENESS OR TIMELINESS OF THE INFORMATION, TEXT, GRAPHICS OR OTHER ITEMS CONTAINED IN THIS COMMUNICATION, AND ALL COMMUNICATIONS IS PRESENTED “AS IS”. THE SENDER EXPRESSLY DISCLAIMS ALL LIABILITY FOR ERRORS OR OMISSIONS IN, OR THE MISUSE OR MISINTERPRETATION OF, ANY INFORMATION CONTAINED IN THIS COMMUNICATION.

Add New Comment